.png)

Seek more insights? Subscribe to our Monthly Newsletter

The United Kingdom is one of the world's leading fintech hubs — home to more fintech unicorns than any other European country, a progressive regulatory environment through the Financial Conduct Authority's innovation programmes, and a financial services ecosystem of global significance centred on London. For international fintech founders seeking to establish a UK-based venture, the fintech visa UK route of choice is overwhelmingly the Innovator Founder Visa.

But fintech applications present specific challenges that generic guidance does not address. The three mandatory criteria: innovative, viable, scalable — are interpreted differently in a financial services context than in a general technology context. Regulatory considerations play a direct role in the viability criterion. The endorsing body landscape includes bodies with specific fintech expertise and others without it. And the evidence that most effectively supports a fintech endorsement application is different from the evidence that works for a deep-tech or creative venture.

This article tailors Innovator Founder Visa guidance specifically to fintech founders.

The Innovator Founder Visa is the primary UK immigration route for international fintech founders for three reasons that are specific to the fintech sector.

Employer independence: A fintech founder building their own company cannot use the Skilled Worker Visa, which requires an employer sponsor, and a founder cannot sponsor themselves. The Global Talent Visa is available to fintech leaders with sufficient sector recognition, but it requires an established track record of recognised leadership rather than the founding of a new venture. The Innovator Founder Visa is specifically designed for founders building new businesses. It is the correct route for the vast majority of international fintech entrepreneurs seeking a UK base.

Speed to market: The UK fintech regulatory environment, including the FCA's regulatory sandbox, innovation pathways, and open banking infrastructure, creates genuine competitive advantages for fintech founders who are physically present in the UK and able to engage directly with regulators, banking partners, and institutional customers. The Innovator Founder Visa provides the immigration status needed to establish that presence.

Settlement pathway: The three-year path to ILR available on the Innovator Founder Visa is faster than most other UK work routes and provides the long-term certainty that fintech founders who are building businesses with multi-year development horizons need.

Eligibility for Fintech Founders

The Three Criteria Through a Fintech Lens

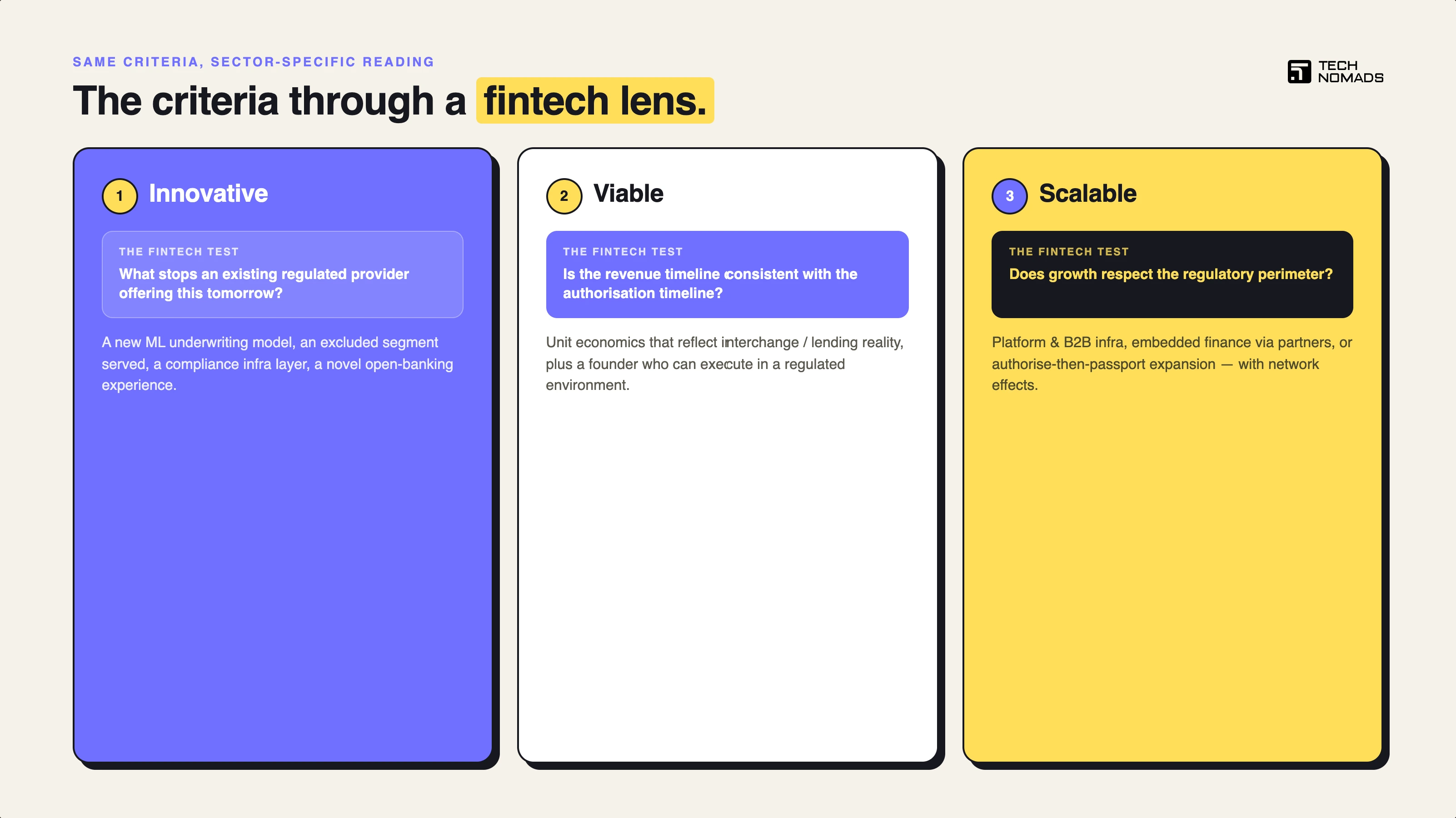

The mandatory criteria for the Innovator Founder Visa: innovative, viable, and scalable, apply to fintech ventures in the same formal terms as to any other sector. What differs is how the endorsing body interprets each criterion through the specific lens of financial services.

Fintech founder profiles that typically succeed combine at least one of the following: deep domain expertise in a specific financial services segment (payments, lending, insurance, wealth management, compliance, infrastructure); a technical background that enables the founder to build the core product without immediate dependency on external engineering resources; or prior fintech industry experience that provides both credibility and a network of potential customers, partners, and recommenders.

The strongest fintech applications typically come from founders who have identified a specific, well-evidenced problem in the financial services ecosystem, often from direct professional experience and who can articulate a differentiated solution with a clear path to regulatory compliance and commercial traction.

Regulatory Considerations and Their Impact on Viability

The financial services sector is one of the most heavily regulated in the UK, and the viable criterion for a fintech venture cannot be assessed without reference to the regulatory framework within which the business will operate.

A payments business requires FCA authorisation or registration. A lending business requires FCA authorisation. An insurance business requires FCA authorisation or, in some cases, a Lloyd's of London market position. A crypto asset business requires FCA registration. A banking business requires PRA and FCA authorisation, the most demanding regulatory pathway in UK financial services.

The business plan for a fintech Innovator Founder Visa application must address the regulatory pathway explicitly. An endorsing body with fintech expertise will ask: what regulatory authorisation does this business require, and what is the founder's plan for obtaining it? A business plan that ignores the regulatory dimension and describes a payments business without acknowledging the FCA authorisation requirement will fail the viability criterion with any endorsing body that understands the sector.

This does not mean the founder must have already obtained regulatory authorisation before applying. Pre-authorisation fintech ventures are entirely eligible. What it means is that the business plan must demonstrate the founder's awareness of and a credible plan for navigating the regulatory pathway. FCA regulatory sandbox participation, engagement with a compliance consultant, or a documented regulatory roadmap all strengthen the viable criterion in this context.

The innovative criterion requires that the business concept is genuinely new, not a replication of an existing model. In fintech, this is a particularly nuanced assessment because the sector has a long history of incremental improvement masquerading as innovation and of genuinely disruptive concepts being dismissed as derivative by assessors who do not understand the specific technical or regulatory differentiation involved.

What constitutes genuine innovation in fintech:

A new technical approach to a persistent financial services problem, for example, applying a genuinely novel machine learning architecture to credit underwriting in a way that produces materially better outcomes than existing approaches, with documented evidence of the performance differential.

A new distribution model that makes financial services accessible to a segment previously excluded or underserved, for example, a lending product specifically designed for the self-employed workforce, with a credit assessment methodology that addresses the income variability that existing lenders cannot accommodate.

A new infrastructure layer that enables other financial services businesses to operate more efficiently or compliantly, for example, an API-based compliance monitoring tool that addresses a specific regulatory requirement that no existing solution adequately covers.

A new application of open banking, embedded finance, or BaaS (Banking as a Service) infrastructure that creates a genuinely new customer experience or product category, for example, a platform that embeds financial services directly into a non-financial customer journey in a way that is not replicable using existing infrastructure.

What does not constitute genuine innovation in fintech:

A mobile banking app that offers the same services as existing challenger banks without a specific differentiating feature. A payments business that processes transactions using existing rails without a specific technical, geographic, or distribution innovation. A lending business that underwrites credit using conventional bureau data without a differentiating assessment methodology. "Better UX" or "lower fees" without a structural explanation for why existing providers cannot replicate the improvement.

The key test for the innovative criterion in fintech is: what specifically prevents an existing regulated financial services provider from offering this product or service tomorrow? If the answer is "nothing they could do if they chose to", the innovative criterion is weak. If the answer is "they would need to rebuild their underwriting model", "they would need to obtain a new regulatory authorisation", or "they would need to integrate with infrastructure they do not currently have access to", the innovative criterion has genuine substance.

What "Viable" Means for a Fintech Business

The viable criterion for a fintech venture encompasses more dimensions than for a typical technology business. The endorsing body is assessing not only whether the business model is commercially credible but also whether the founder has the specific capability to execute in a regulated environment.

Commercial viability in fintech:

The business plan must demonstrate a credible path to revenue that is consistent with the regulatory authorisation timeline. A payments business that projects revenue from month three must explain how it will be processing payments without FCA authorisation or must demonstrate that authorisation will be obtained within that timeframe. Commercially unrealistic timelines relative to the regulatory pathway are a common source of failure on the viability criterion.

The unit economics of the fintech business must be coherent. A lending business with a customer acquisition cost that exceeds the lifetime value of a typical loan is not viable. A payments business that projects margins without reference to interchange economics is not viable. The endorsing body's expert assessors in the fintech space will assess the financial model against their knowledge of sector economics. Generic projections that do not reflect the specific economics of the fintech vertical will not survive this scrutiny.

Founder viability in fintech:

The founder must demonstrate the specific capability required to build and operate a regulated financial services business. This typically requires one or more of: prior employment in financial services at a level that demonstrates understanding of the regulatory environment; a technical background that enables the founder to build the core product; a co-founder or adviser with the financial services expertise the primary founder lacks; or documented engagement with FCA innovation pathways that demonstrates the founder is actively navigating the regulatory dimension.

Scalability in fintech has a specific meaning that differs from scalability in pure software businesses. The endorsing body will assess whether the business model is capable of significant growth, but it will also assess whether that growth model is consistent with the regulatory constraints of the sector.

A fintech business that is regulated must obtain regulatory authorisation before it can scale beyond certain thresholds. A business that proposes to scale rapidly without acknowledging the authorisation constraints or that proposes to operate outside the regulatory perimeter is presenting an unrealistic scalability model.

The most credible scalability models for fintech ventures include:

Platform models: A fintech that provides infrastructure or tooling to other financial services businesses can scale by adding clients without proportionally increasing its own regulatory complexity. API-first products, compliance infrastructure, and B2B fintech platforms are inherently scalable in this way.

Embedded finance models: A fintech whose product is distributed through non-financial partners, such as retailers, HR platforms, and healthcare providers, can access scale through its partners' existing customer bases without building its own distribution from scratch.

Regulatory-ready expansion models: A fintech that obtains authorisation in the UK and plans to expand into other jurisdictions using a clear regulatory strategy, for example, an EMI licence in the UK followed by European passporting or equivalent arrangements, is presenting a scalability model that acknowledges regulatory reality while demonstrating genuine growth potential.

Network effect models: A payments business, a marketplace lending platform, or a peer-to-peer financial service that benefits from network effects, where the platform becomes more valuable as more participants join, has a structurally scalable model that the endorsing body can assess against comparable fintech business cases.

FCA Engagement and Regulatory Sandbox Participation

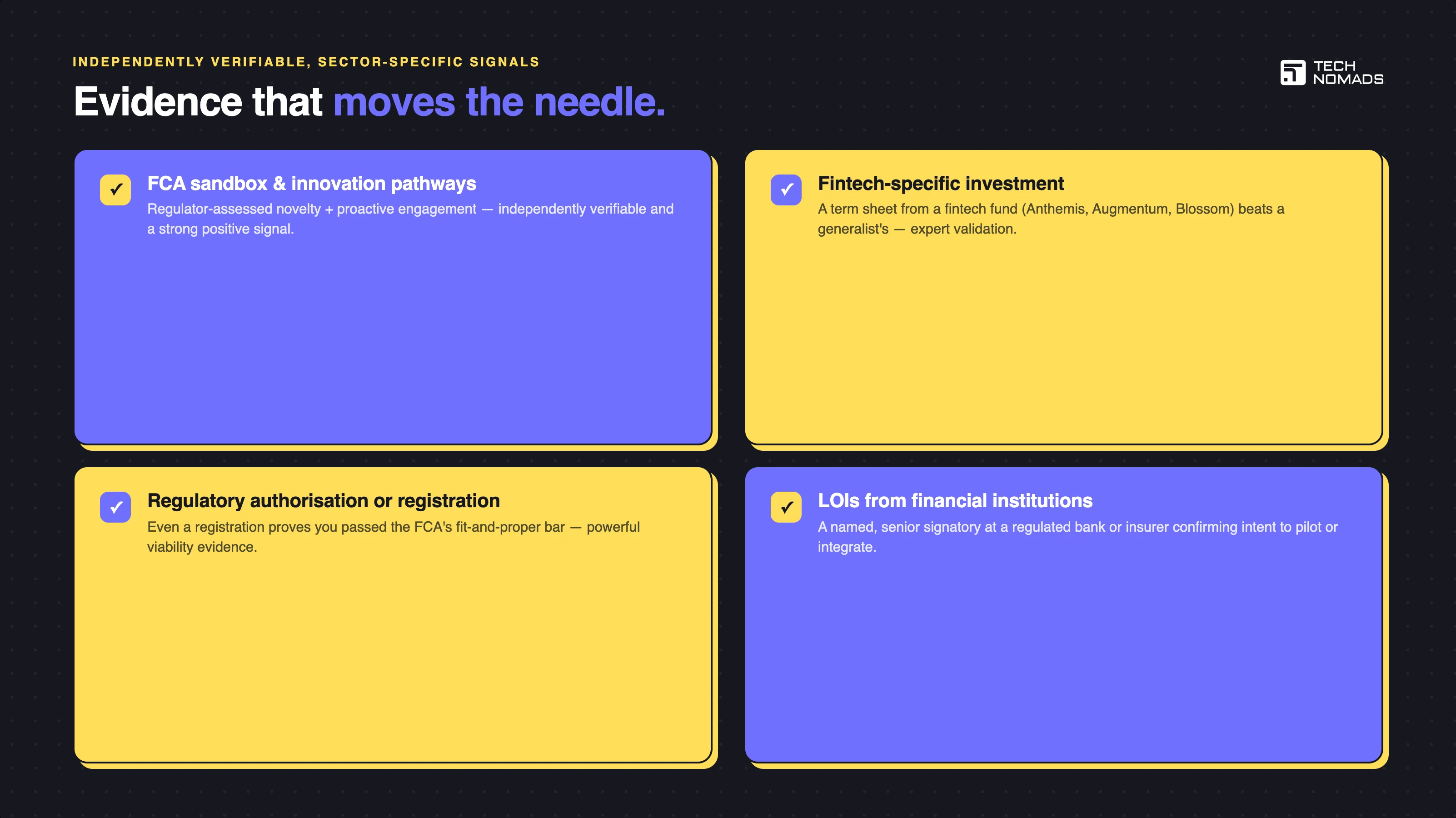

Engagement with the FCA's innovation pathways — particularly the FCA Regulatory Sandbox or the FCA Innovation Pathways service is among the most powerful evidence available to a fintech Innovator Founder Visa applicant. It demonstrates simultaneously that the concept has been assessed by the UK's financial regulator as meriting dedicated innovation support; that the founder has engaged proactively with the regulatory dimension of the business; and that the concept is innovative enough to qualify for a programme specifically designed for genuinely novel financial products.

FCA Regulatory Sandbox participation letters, Innovation Pathways engagement documentation, and Digital Sandbox access confirmation are all independently verifiable and carry significant weight with endorsing bodies that understand the fintech sector. Not all fintech ventures will qualify for sandbox participation, and the absence of sandbox engagement does not weaken the application, but its presence is a significant positive signal.

(Source: FCA Innovation — fca.org.uk)

Investment and Traction Evidence Specific to Fintech

Fintech-specific investment signals carry particular weight because fintech investors are sophisticated assessors of both the commercial and regulatory dimensions of a venture. A term sheet or investment letter from a recognised fintech-focused fund: Anthemis, Augmentum Fintech, Blossom Capital, or similar, is more compelling than the equivalent from a general technology investor, because it signals that an expert in the specific sector has assessed and validated the concept.

Regulatory authorisation itself, even a registration rather than a full authorisation, is powerful evidence of viability, as it demonstrates that the business has passed the FCA's fit and proper assessment and met the minimum requirements for operating in the regulated space.

Early revenue from institutional or corporate customers: banks, insurance companies, asset managers carries more weight than equivalent consumer revenue in most fintech applications, because institutional customer acquisition demonstrates that sophisticated, regulated counterparties have assessed and accepted the product.

Letters of Intent from Financial Institutions

Letters of intent from financial institutions: banks, insurance companies, payment processors, or other regulated entities are among the strongest available evidence for the viable criterion in a fintech application. A letter from a named, regulated financial institution confirming their intent to pilot, integrate, or purchase the fintech product demonstrates that a sophisticated, regulated counterparty has evaluated the concept and found it credible.

These letters should be specific, naming the product, the proposed commercial arrangement, and the timeline and should come from a sufficiently senior signatory at the institution to be credible. A letter from the head of innovation or the chief digital officer at a mid-sized UK bank carries significantly more weight than a letter from a junior relationship manager.

The choice of endorsing body is particularly important for fintech applications because the three mandatory criteria have significant sector-specific dimensions that an assessor without fintech expertise may not be well-positioned to evaluate.

Technology-focused endorsing bodies with fintech expertise, accelerators and programmes that have previously endorsed fintech ventures are the most natural fit for most fintech Innovator Founder Visa applications. The portfolio alignment matters: an endorsing body that has previously endorsed payments businesses, lending platforms, or compliance technology ventures has developed the expertise to assess your concept credibly and the portfolio context to appreciate its differentiation.

Endorsing bodies with financial services sector expertise, including some bank-backed innovation programmes and financial services industry bodies, are appropriate for fintech ventures with a strong institutional dimension, where the endorsing body's relationships with financial institutions may add value beyond the endorsement itself.

General endorsing bodies, including Innovate UK, are appropriate for cross-sector fintech ventures or for concepts that sit at the intersection of financial services and another sector (for example, climate fintech or health payments). Innovate UK's grant funding track record is particularly relevant for fintech ventures with a technology innovation dimension, as an existing Innovate UK grant is both powerful evidence for the innovative criterion and a signal of alignment between the venture and the endorsing body's portfolio.

Claiming Innovation Without Regulatory Differentiation

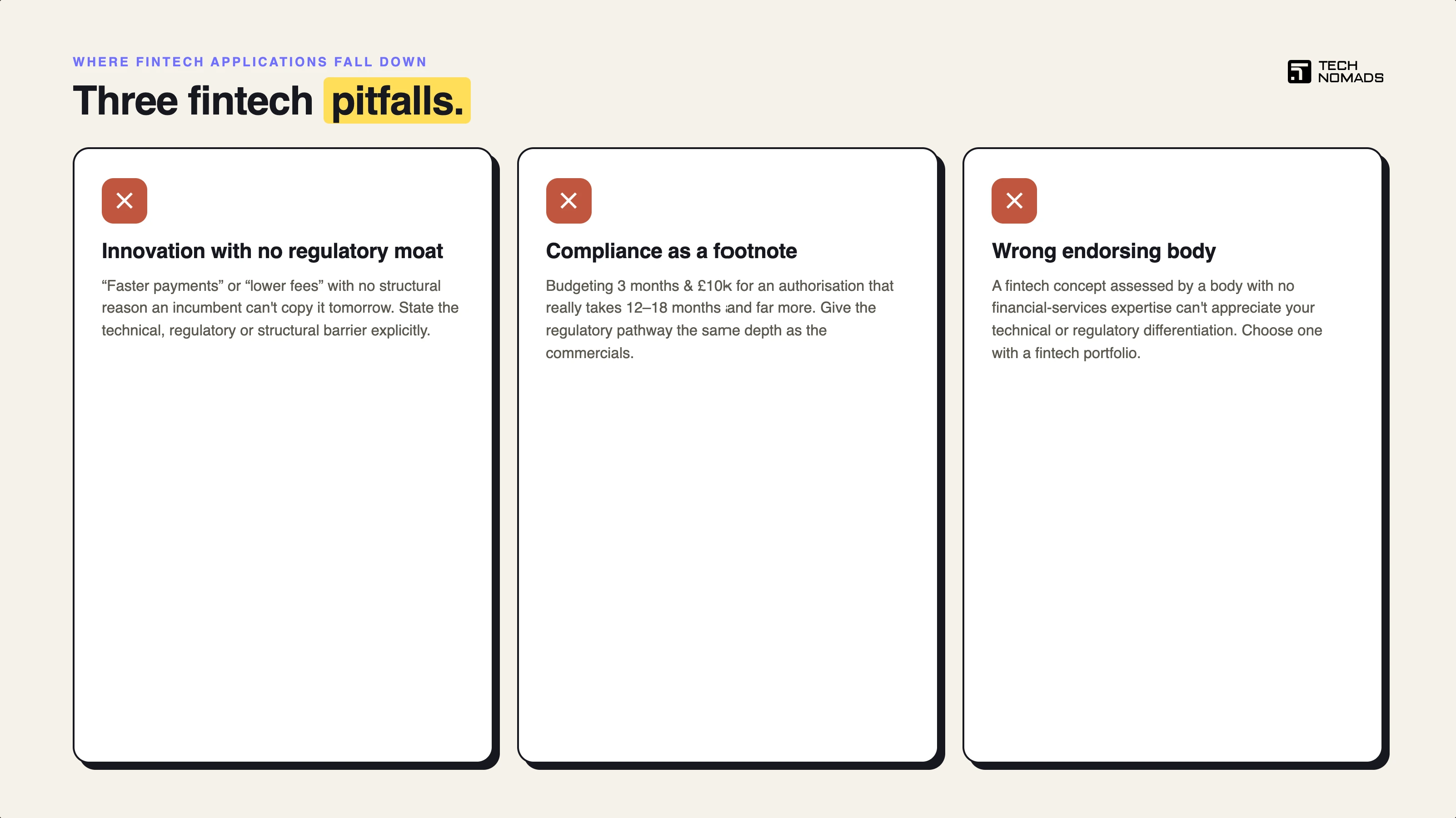

The most common fintech-specific pitfall is asserting innovation without explaining why the innovation is not simply replicable by an existing regulated provider. A fintech that offers "faster payments" or "lower fees" without explaining the structural mechanism by which it achieves those outcomes and why existing providers cannot replicate them, is not presenting a credible innovative criterion argument.

The innovative criterion for a fintech venture must address the regulatory dimension directly. If your product is genuinely innovative, there is a regulatory, technical, or structural reason why existing providers cannot simply copy it. That reason should be stated explicitly in the business plan and personal statement.

Underestimating the Compliance Dimension of Viability

The second most common fintech-specific pitfall is a business plan that treats regulatory compliance as a footnote rather than a central operational challenge. A payments business that allocates three months and £10,000 to FCA authorisation when the actual timeline is twelve to eighteen months, and the cost is significantly higher, is presenting a financially and operationally unrealistic plan.

The compliance dimension of viability should be addressed with the same depth as the commercial dimension. The plan should specify which regulatory authorisations are required, the realistic timeline for obtaining them, the associated costs, and the founder's plan for managing the business during the pre-authorisation period.

Applying to an Endorsing Body Without Fintech Expertise

A fintech application submitted to an endorsing body without specific financial services expertise is at risk of being assessed by assessors who cannot evaluate the innovative and viable criteria with the sector-specific knowledge those criteria require in this context. The endorsing body's inability to appreciate the technical or regulatory differentiation of your concept is not a basis for appeal; it is a risk that should be mitigated by choosing a body with demonstrated fintech expertise.

How Tech Nomads Positions Fintech Applications

Tech Nomads has specific experience supporting fintech Innovator Founder Visa applicants, including founders building in payments, lending, compliance technology, wealth management, and embedded finance. The team understands the sector-specific interpretation of the mandatory criteria and works with fintech founders to build applications that address the regulatory dimension of viability, articulate the structural basis for innovation, and present a scalability model that is consistent with the realities of the regulated financial services environment.

Tech Nomads is a global mobility platform that provides services for international relocation. Established in 2018, Tech Nomads has a track record of successfully relocating talents and teams. Our expertise in adapting to regulatory changes ensures our clients’ satisfaction and success.

Tech Nomads Club

Tech Nomads Club is a curated global community for highly skilled professionals.

We host free, application-based events, including expert panel talks, start-up pitch days, members-only networking, informal meetups, and fireside conversations with industry leaders.

Membership is free but selective — open to those building across borders and seeking meaningful growth through connection, knowledge, and community.

We also produce a regular podcast that shares real stories, insights, and voices from inside the Club.

Book a Consultation

Ready to find out whether the UK Global Talent Visa (Arts & Culture) is the right route for your profile?

To explore your UK relocation options, you may:

Subscribe to our social media platforms to stay up-to-date on global mobility news and opportunities:

Useful Resources:

Information made available on this website in any form is for information purposes only. It is not, and should not be taken as advice. You should not rely on, or take or fail to take any action based upon this information.

© Copyright 2024, All Rights Reserved

.png)

.png)

.png)

.avif)

.png)